The survey, conducted for the Asian Trader Symbol, Fascia & Franchise Supplement, captured a broad cross-section of UK convenience and forecourt retailers, spanning major symbol groups including Londis (20%), Premier (16.7%), Costcutter (18.3%), Budgens (15%), SPAR (11.7%) and Nisa (6.7%), alongside independent stores.

Two-thirds of the respondents (68%) were part of a symbol group, 11% belonged to fascia or franchise, and the rest (21%) were unaffiliated independents.

Around 70% of affiliated respondents have been with their group for more than three years. The profile remains core UK convenience: predominantly single-store operators (70.4%). Nearly one in four (23.4%) owned 2-5 stores, and the rest six or more.

The core value equation

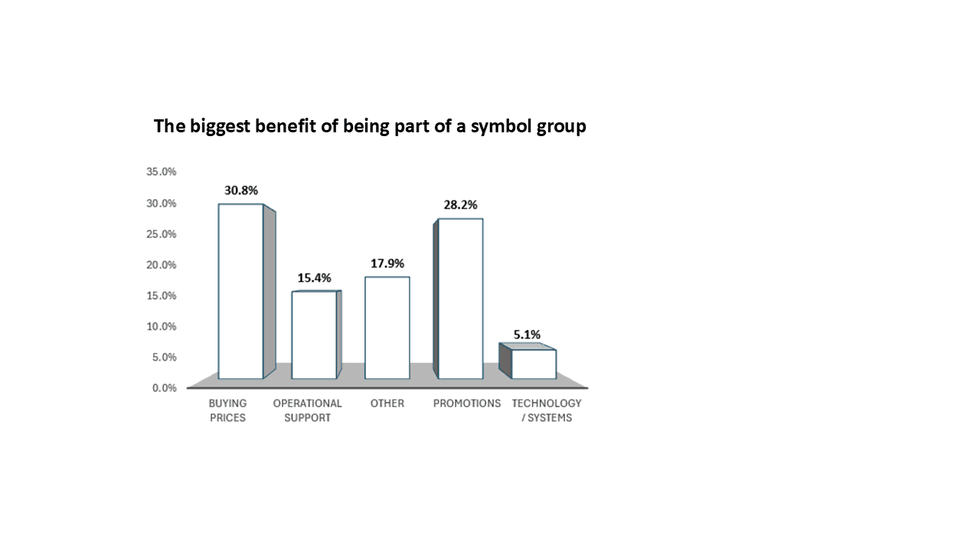

When asked about the biggest benefit of group membership, buying power and promotions emerged clearly as the dominant themes.

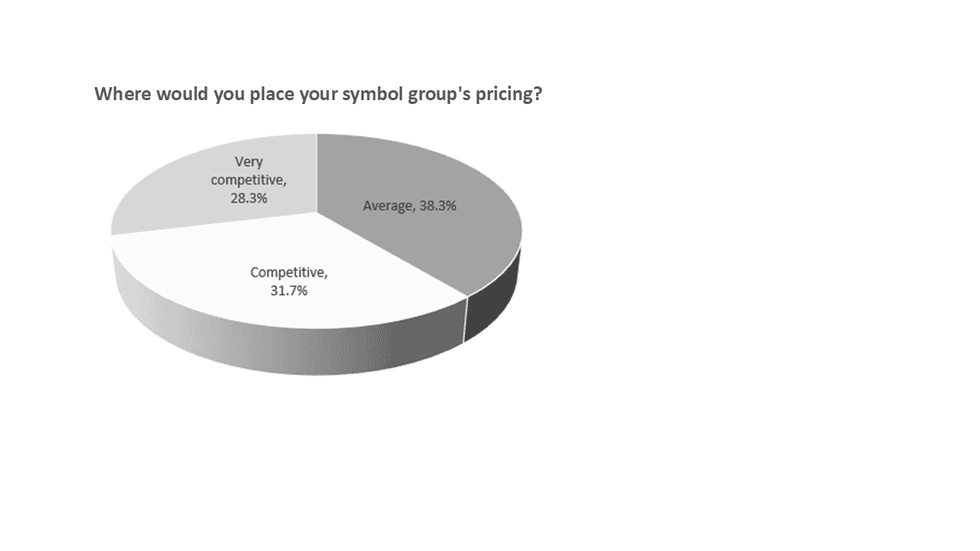

Pricing perception is strongly positive:

- Around 60% rate their group’s pricing as competitive or very competitive.

- Nearly three-quarters say membership helps both protect margins and drive volume, rather than forcing a trade-off.

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

In terms of profit drivers, alcohol leads as the primary profit category (41.3%), followed by tobacco/vapes (23.9%).

Importantly, the data suggests most retailers feel their group delivers a balanced commercial model – supporting both top-line growth and bottom-line protection.

The operational test

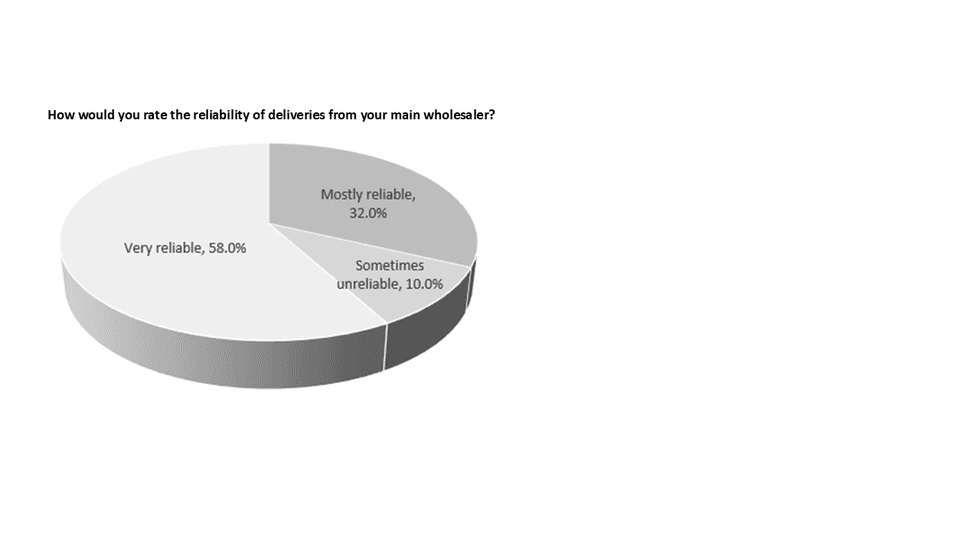

Delivery reliability scores well overall, but this is also where frustration concentrates.

Key findings:

- Most retailers rate delivery reliability positively, 58% saying “very reliable” and 32% as “mostly reliable”.

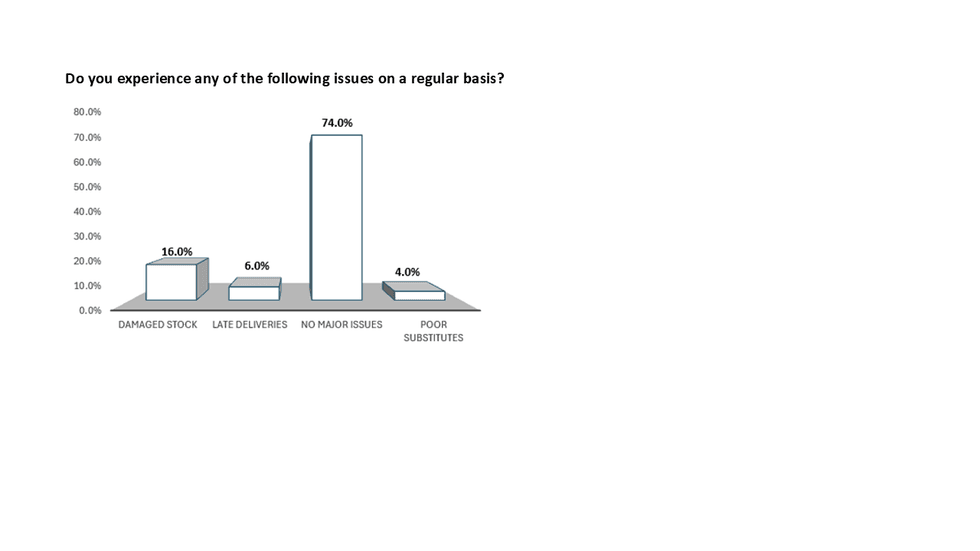

- Damaged stock is the single biggest pain point, cited by 16% of respondents.

- Common concerns include late deliveries and poor substitutes.

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

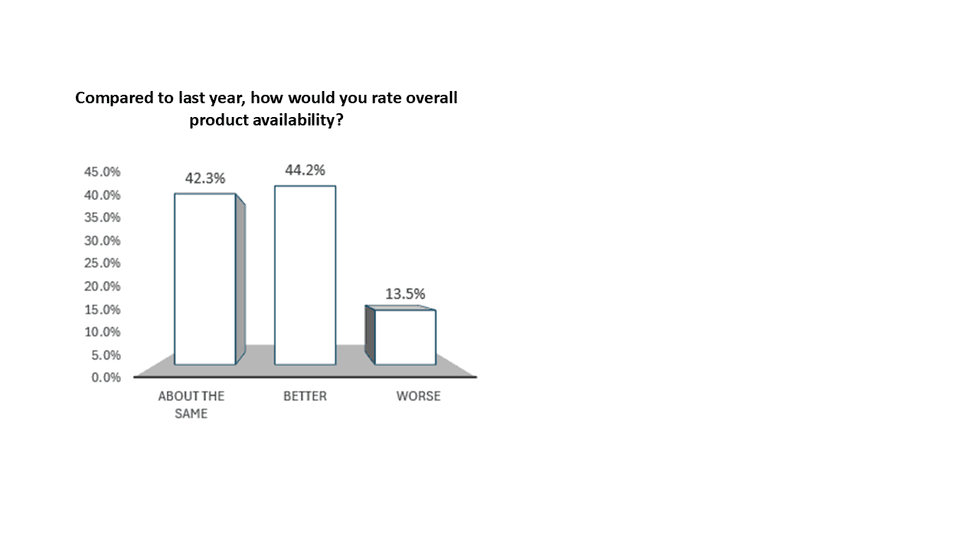

Compared to last year:

- Availability is broadly stable (42.3%) or improved (44.2%) for most.

- There is no widespread crisis sentiment, but service consistency clearly matters.

On own brand:

- The majority say own-brand plays a big (53.8%) or meaningful (28.8%) role in their sales.

- Quality is generally rated comparable to supermarket own-label, with two in five (42.3%) saying they are better than the supermarket offerings.

- Most feel groups are introducing NPD quickly enough to remain competitive.

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Planograms and ranging are also largely seen as aligned with shopper needs (84.3%), suggesting reasonable central merchandising support.

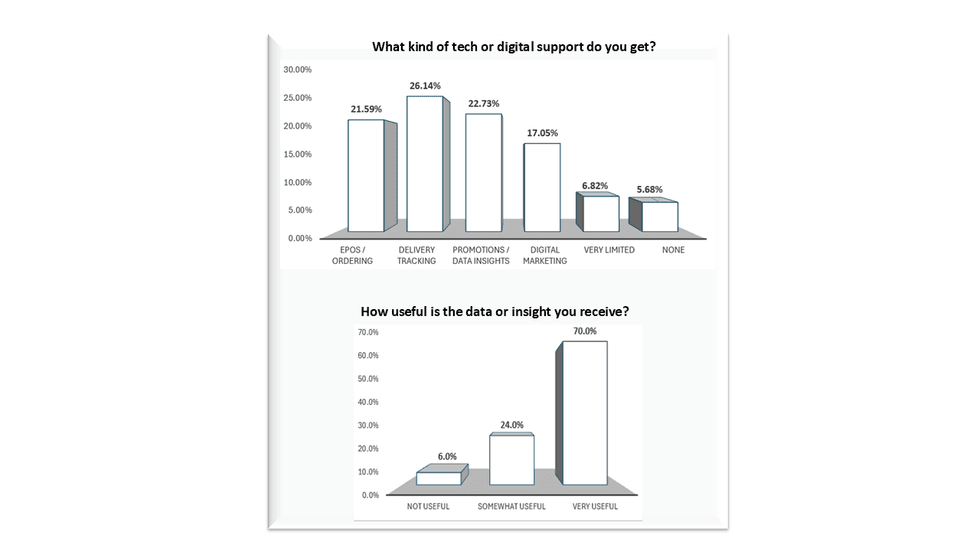

Tech and people support

Retailers report receiving a range of support, including delivery tracking (26.14%), EPOS/ordering systems (21.59%), promotions/insights (22.73%) and digital marketing (17.05%).

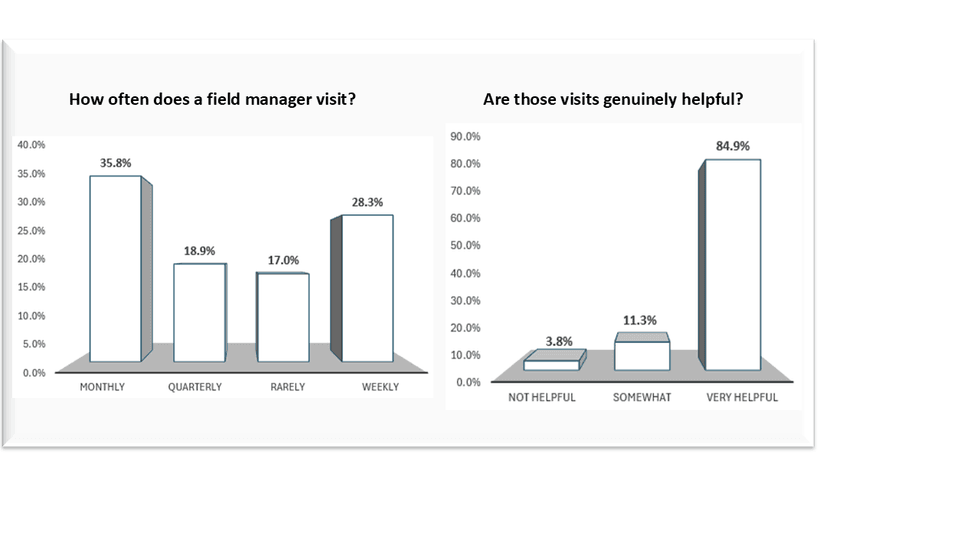

Field manager visit frequency varies, but most report regular visits – only 17% say the visits are rare – and generally find them very helpful (84.9%) in improving execution and store standards.

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

However, insight support is more variable, with 70% seeing it as very useful while 24% say somewhat useful. This suggests potential opportunity for deeper commercial analytics or more actionable insights.

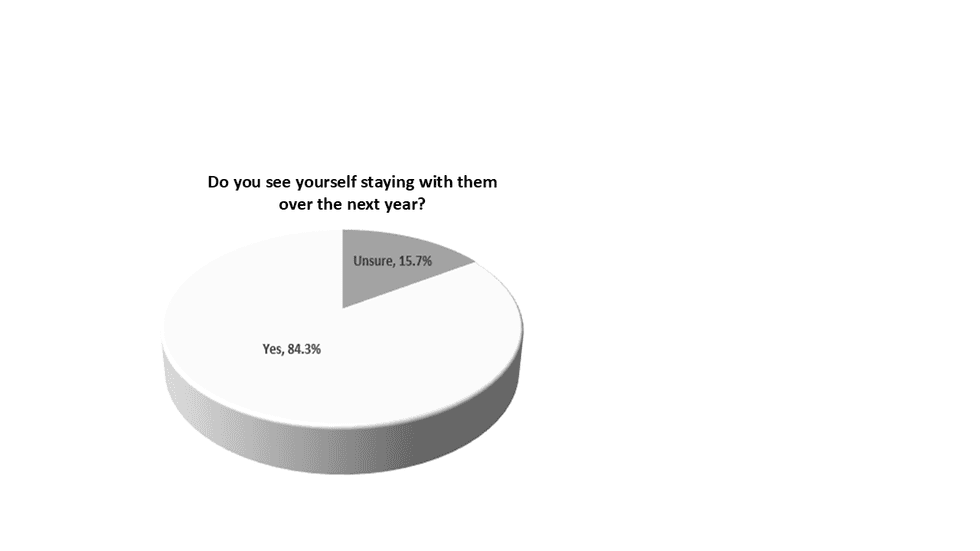

Strong loyalty, with a caveat

The loyalty signal is unmistakable:

- More than 84% intend to stay with their group over the next year.

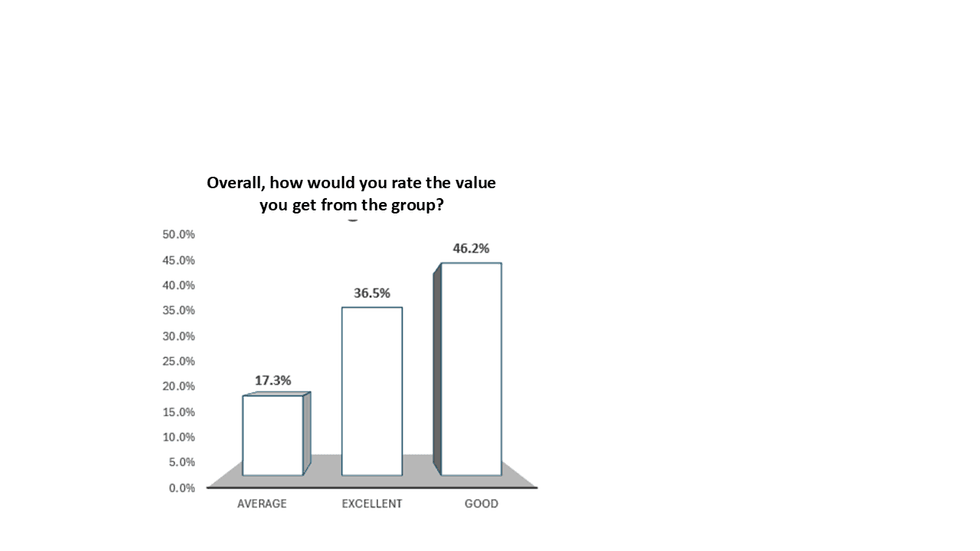

- Over 80% rate overall value as good or excellent.

This represents a high level of endorsement across the sector.

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

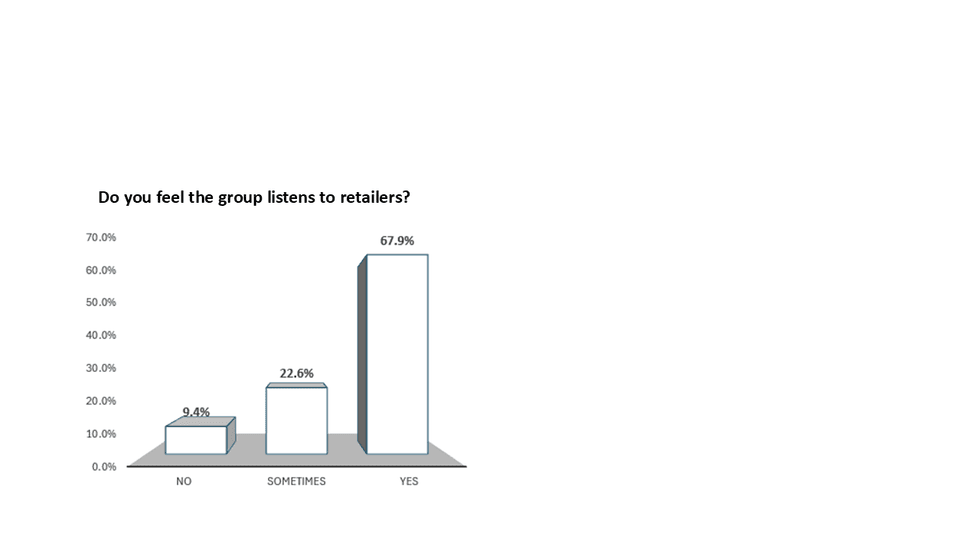

However, one tension point stands out. Around one in three retailers feel their group only sometimes (22.6%) – or does not (9.4%) – listen to them.

This “listening gap” does not currently translate into mass switching risk – but it is a clear relational pressure point.

Photo: Asian Trader

Photo: Asian Trader

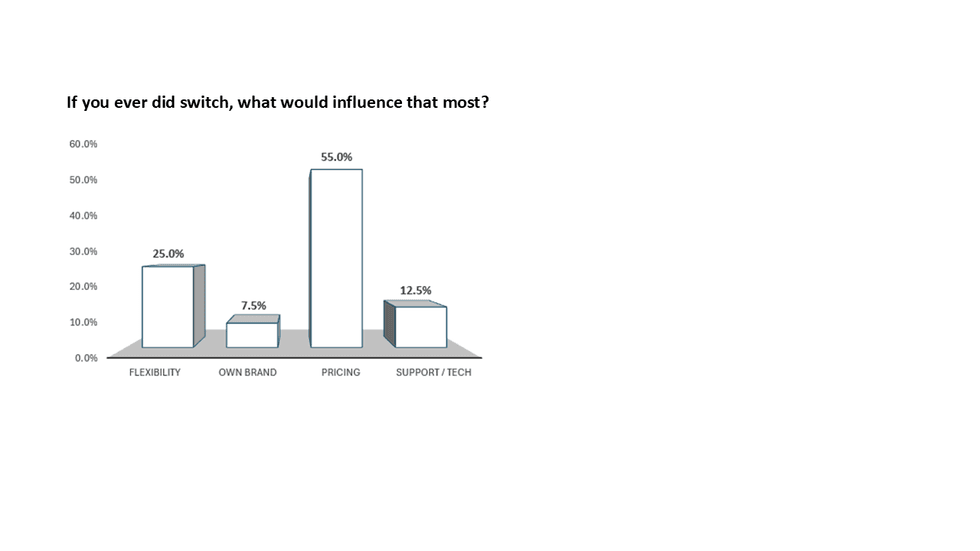

When asked what would trigger a switch, pricing dominates overwhelmingly (55%), far ahead of own brand (7.5%), flexibility (25%), support/tech concerns (12.5%).

Commercial competitiveness remains king.

Biggest Benefits v Biggest Frustrations

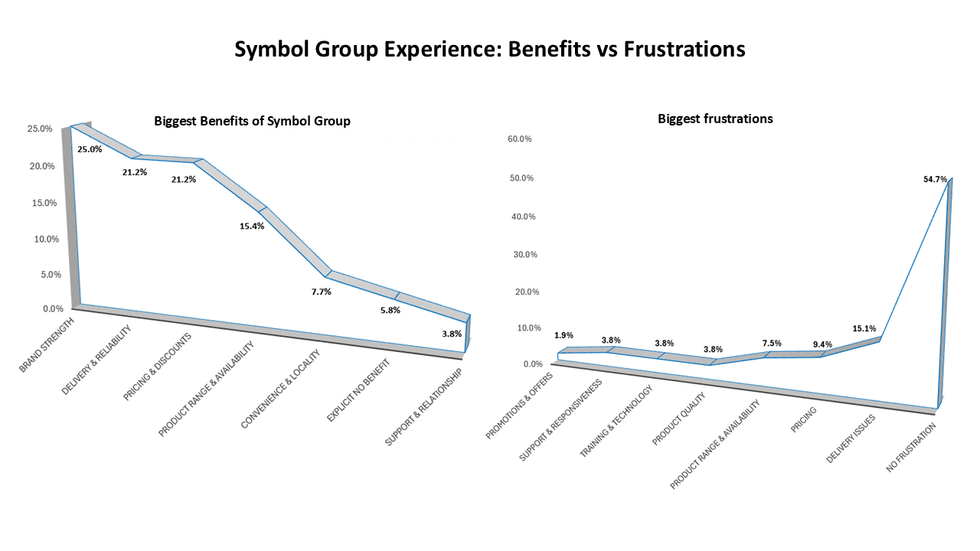

Top Benefits Identified

- 1.Brand strength (25%)

- 2.Delivery reliability (21.2%)

- 3.Pricing & discounts (21.2%)

- 4.Range and availability (15.4%)

Photo: Asian Trader

Photo: Asian Trader

Very few retailers say they see “no benefit” from symbol membership – reinforcing its continued relevance.

Top Frustrations

- 54.7% report no major frustrations

- 15.1% cite delivery issues

- 9.4% cite pricing concerns

- All other issues are fragmented and low frequency (below 8%)

Overall, this is a broadly positive retailer experience picture, with service execution – not structural dissatisfaction – driving complaint.

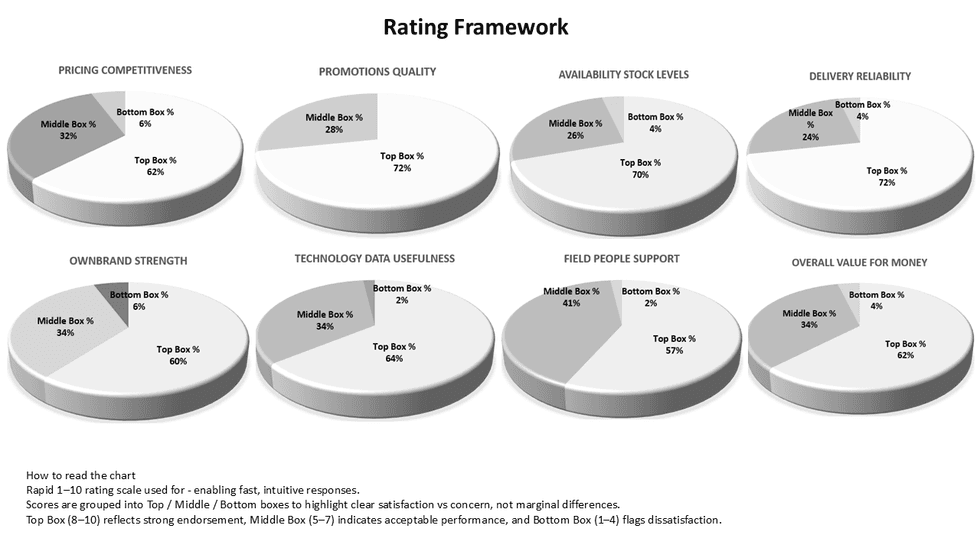

The rating framework

Retailers scored various areas on a rapid 1–10 scale.

Scores were grouped into:

- Top Box (8–10): Strong endorsement

- Middle Box (5–7): Acceptable performance

- Bottom Box (1–4): Dissatisfaction

Photo: Asian Trader

Photo: Asian Trader

This approach highlights meaningful satisfaction gaps rather than marginal differences.

The clustering leans heavily toward Top and Middle boxes across most operational measures, reinforcing the overall stability of the symbol model.

The average rating for each area is:

- Pricing Competitiveness: 7.5

- Promotions Quality: 8.2

- Stick Availability: 8.1

- Delivery Reliability: 8.3

- Own-brand Strength: 7.8

- Tech/Data Usefulness: 7.9

- Filed/People Support: 7.9

- Overall Value for Money: 7.9

The independent perspective

Alongside affiliated retailers, unaffiliated independents offered insight into barriers and triggers.

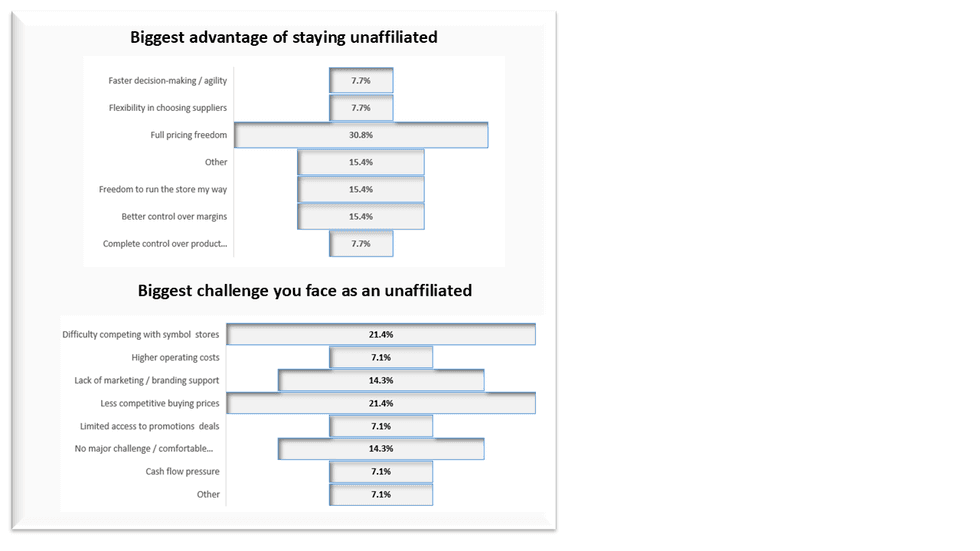

Pricing freedom (30.8%) has been cited as the biggest advantage of staying independent, followed by the freedom to “run the store my way” (15.4%) and better control over margins (15.4 per cent). Flexibility in sourcing, faster decision-making and complete control over ranging also found mention.

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Photo: Asian Trader

Interestingly, the competition from the symbol stores (21.4%), along with weak buying power, is the biggest challenge these stores now face. Lack of marketing support (14.3%) and limited access to promotional deals (7.1%) also figure among the challenges.

They also report higher operating costs and cashflow pressures, indicating that the impact of the wider issues affecting the sector is much more pronounced among this cohort.

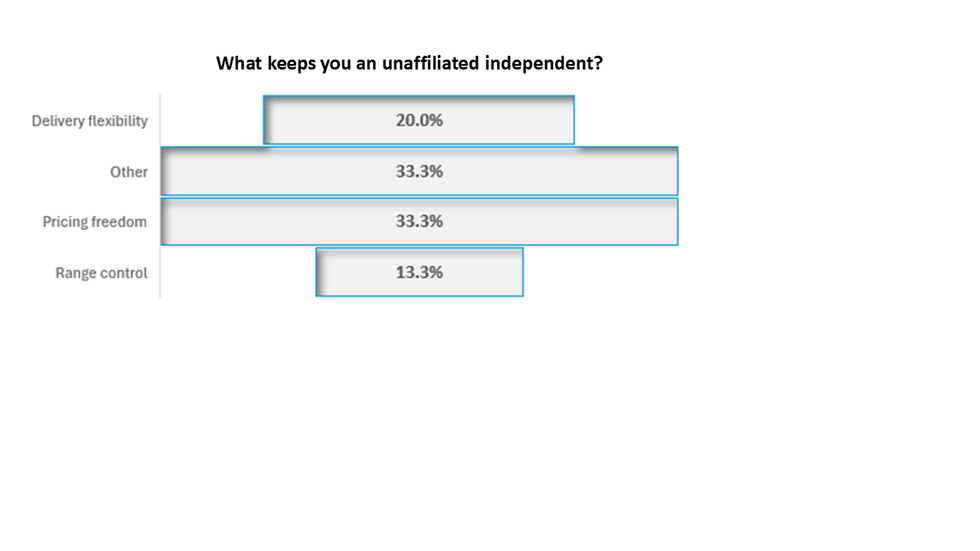

Yet, when asked whether they would consider joining a symbol or fascia, only 13.3 per cent were receptive. Others remain cautious due to contract concerns or perceived loss of autonomy.

What must improve to attract independents?

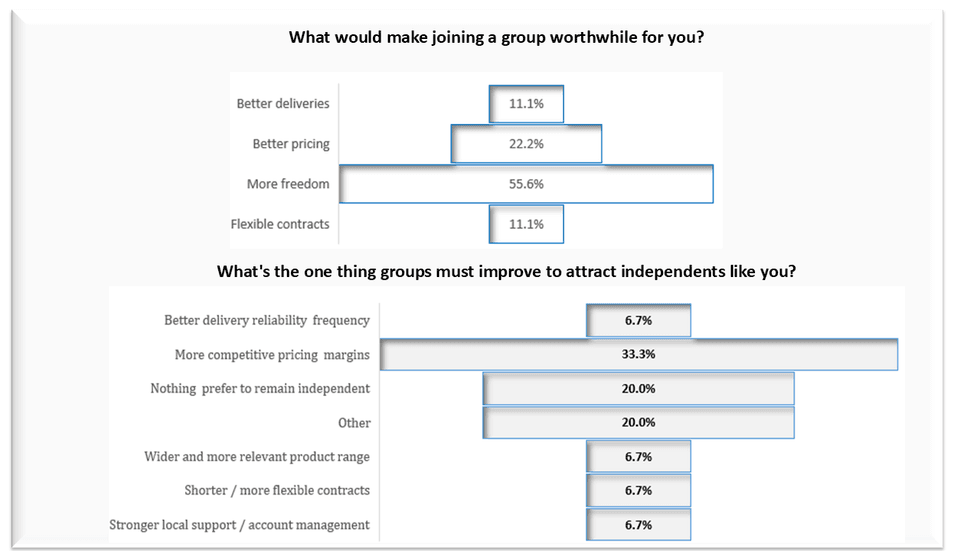

Competitive pricing stands out as the single biggest lever for change, with 33.3% of independents saying sharper pricing would be the key factor in persuading them to join a symbol group.

However, the data also reveals a hard ceiling. One in five independents say nothing would change their decision to remain unaffiliated, underlining the deep-rooted value placed on autonomy, flexibility and full control over range and pricing.

Photo: Asian Trader

Photo: Asian Trader

For symbol groups, the implication is twofold: while pricing remains the most powerful recruitment tool, there will always be a core segment of retailers for whom independence is not a stepping-stone – but a strategic choice.

The big picture

The 2026 retailer pulse suggests a sector that is:

- Commercially stable

- Operationally functional

- Largely loyal

- But sensitive to pricing shifts

Symbol and fascia groups continue to anchor the UK convenience backbone through brand strength, buying scale and structured support.

Yet the competitive battleground remains uncompromising.

If pricing perception weakens – or if delivery reliability slips – loyalty could be tested quickly.

For now, however, the data shows a sector that remains confident in the symbol model – with pricing competitiveness and operational consistency the two pillars holding it firmly in place.