As consumers increasingly seek healthier, more functional food and drink options, sports and protein products are becoming an established fixture in convenience retail. Exclusive research by Zebra Stripes for Asian Trader reveals a category enjoying broad shopper appeal, stable retailer support and continued sales momentum.

Read category feature: Powered up and cashing in

The survey of convenience retailers highlights how the sector has moved beyond its traditional fitness roots. General shoppers now represent the biggest source of demand, while convenient grab-and-go formats such as protein bars and ready-to-drink products are driving sales across the channel.

Perhaps most tellingly, retailers view the category as a dependable part of their offer. The overwhelming majority are maintaining or growing their ranges, suggesting sports and protein products have secured their place within the modern convenience store.

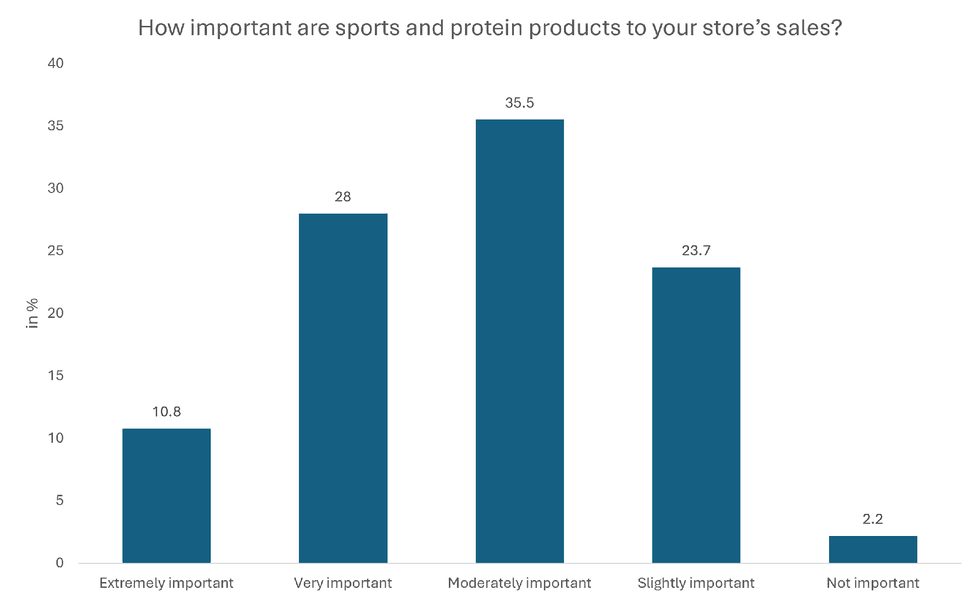

An important category for many stores

The findings suggest that sports and protein products are making a meaningful contribution to convenience store sales. Nearly six in ten retailers (59.2 per cent) describe the category as at least moderately important to their business, while almost four in ten (38.8 per cent) say it is either very important or extremely important.

Photo: Asian Trader

Photo: Asian Trader

The largest group of respondents (35.5 per cent) regard sports and protein products as moderately important, highlighting a category that has become a steady contributor rather than a specialist sideline.

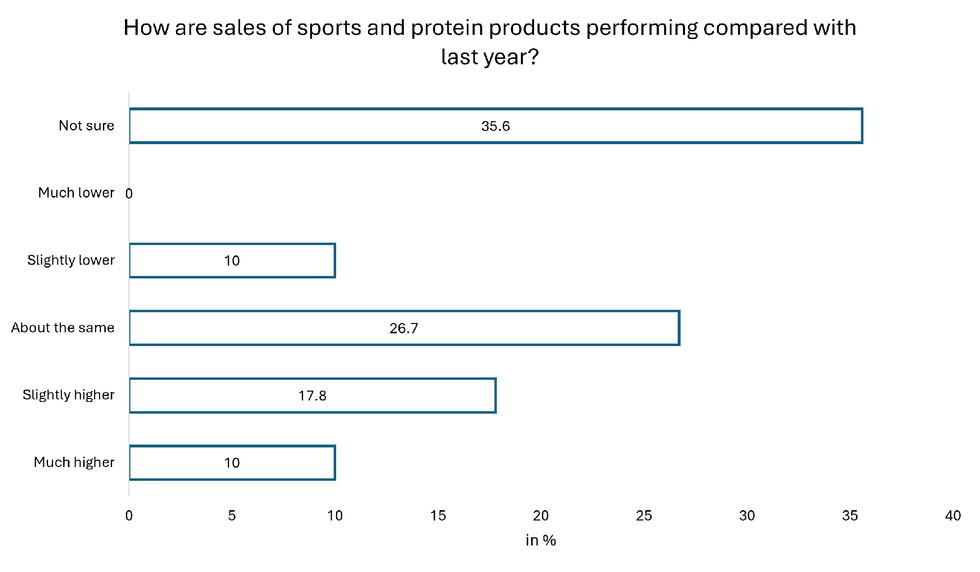

Stable growth momentum

When asked how sales are performing compared with last year, retailer responses suggest a market characterised by resilience and steady progress.

Although 35.6 per cent of respondents were unsure about year-on-year performance, among those able to assess trends the outlook was positive. More than a quarter (27.8 per cent) reported higher sales than a year ago, including 10 per cent who said sales were much higher.

Photo: Asian Trader

Photo: Asian Trader

Meanwhile, 26.7 per cent said sales were broadly unchanged, while only 10 per cent reported a slight decline. Notably, none of the retailers surveyed reported a significant drop in sales.

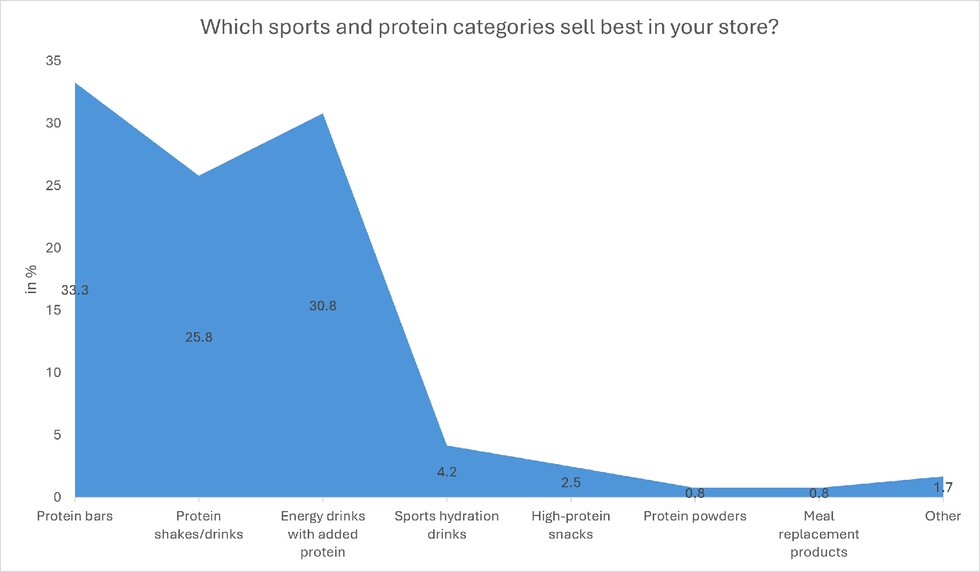

Protein bars lead the way

Among the various sports nutrition segments, protein bars remain the standout performer.

One-third of retailers (33.3 per cent) identified protein bars as their best-selling sports and protein category, ahead of protein-enhanced drinks and shakes.

The results reflect wider consumer trends favouring portable, convenient products that can be consumed on the move, whether as a snack, meal accompaniment or post-workout option.

Photo: Asian Trader

Photo: Asian Trader

Protein shakes and ready-to-drink products also continue to perform strongly, demonstrating growing demand for convenient protein solutions that require no preparation.

More specialist segments such as protein powders, meal replacements and sports hydration products achieved much lower responses, reinforcing the convenience channel's focus on grab-and-go formats rather than products associated with dedicated sports nutrition retailing.

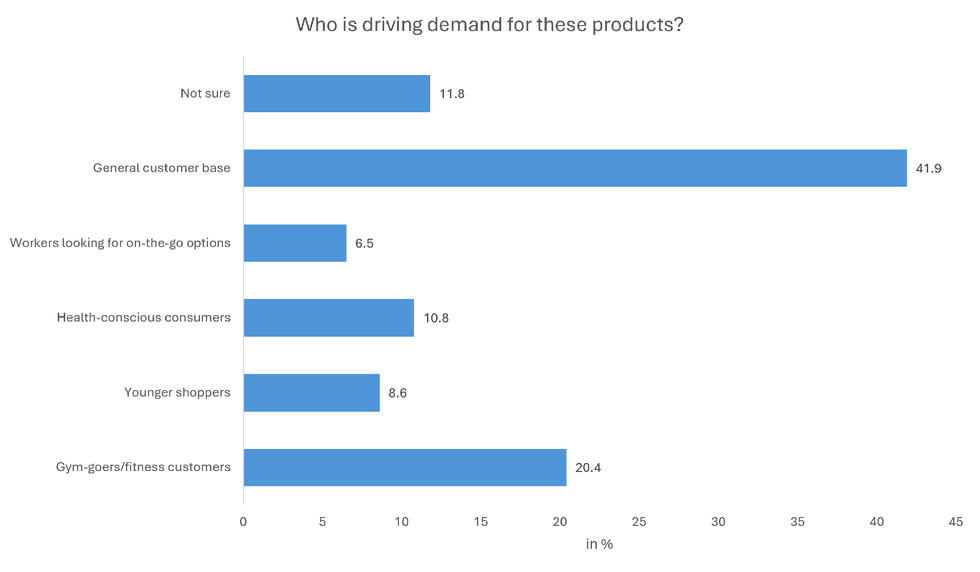

Mainstream appeal widens

Perhaps the most significant finding is the extent to which sports and protein products have entered the mainstream.

The survey shows that general shoppers are now the biggest driver of category demand, accounting for 41.9 per cent of responses.

Photo: Asian Trader

Photo: Asian Trader

While gym-goers and fitness-focused consumers remain an important audience, representing 20.4 per cent of demand, they are no longer the dominant customer group.

Health-conscious shoppers were cited by 10.8 per cent of respondents, while younger consumers and workers seeking convenient nutrition options also featured among key demand drivers.

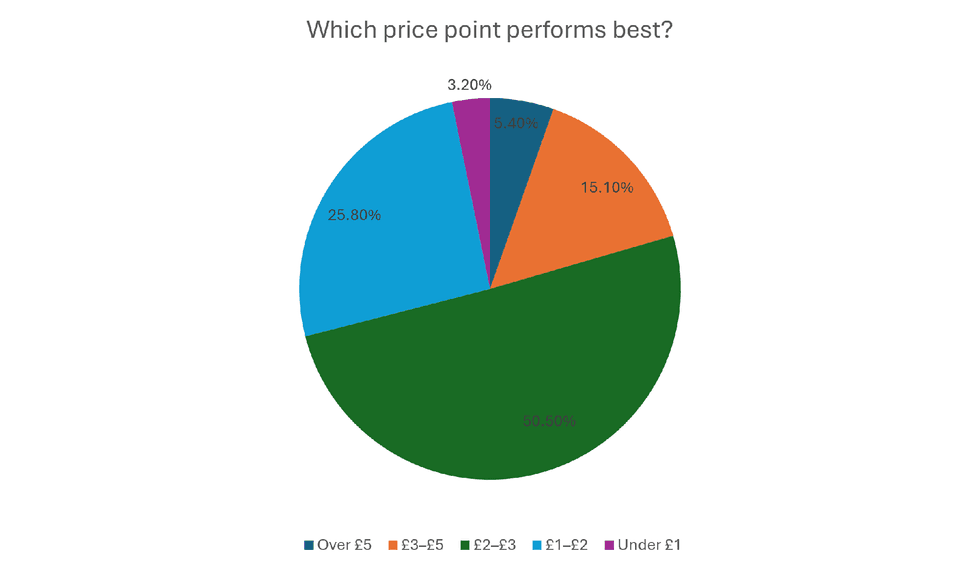

Hitting the sweet spot on price

Price remains a crucial factor in driving category performance.

Half of all respondents (50.5 per cent) identified the £2-£3 price bracket as the strongest-performing range for sports and protein products, making it the clear sweet spot for shoppers.

A further 25.8 per cent highlighted products priced between £1 and £2, meaning more than three-quarters of retailers see the greatest success within the £1-£3 range.

Photo: Asian Trader

Photo: Asian Trader

Higher-priced products showed progressively lower levels of performance, suggesting that while shoppers are willing to pay a premium for functional nutrition, affordability remains critical within convenience retail.

The findings provide a useful benchmark for retailers reviewing their ranging and pricing strategies, particularly as cost pressures continue to influence purchasing decisions.

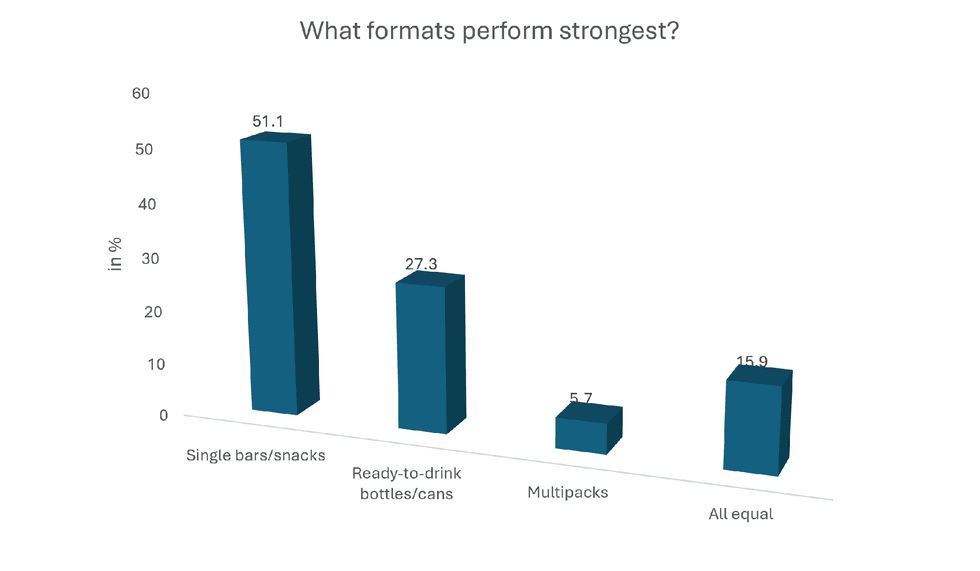

Convenience remains king

The dominance of convenience-led formats is another recurring theme throughout the survey.

More than half of retailers (51.1 per cent) identified single bars and snacks as the strongest-performing format in the category. Ready-to-drink bottles and cans followed at 27.3 per cent.

Photo: Asian Trader

Photo: Asian Trader

In contrast, larger formats such as multipacks attracted limited support, while powders and tubs generated virtually no demand.

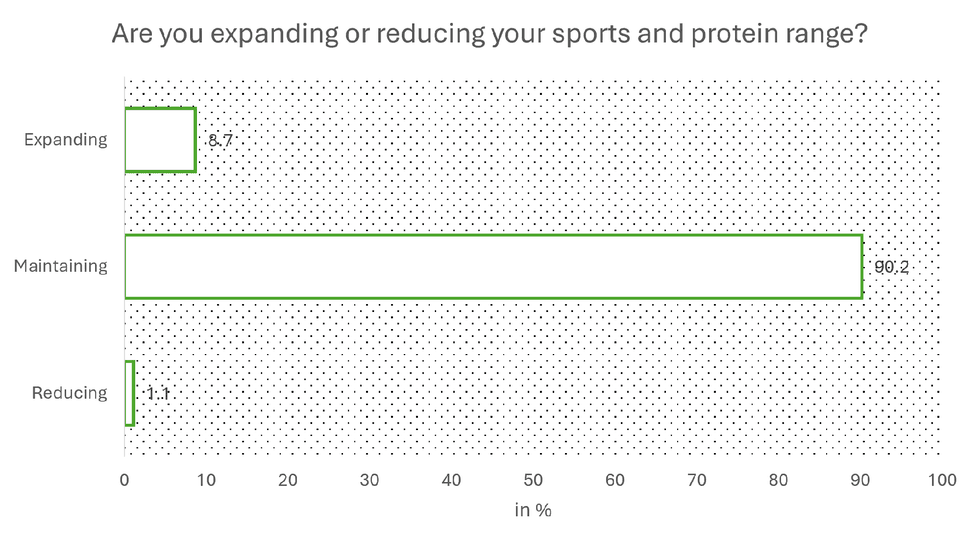

Retailers backing the category

One of the most encouraging findings for brands operating in the sector is the level of retailer commitment.

An overwhelming 90.2 per cent of respondents said they are maintaining their current sports and protein range, demonstrating confidence in the category's ongoing role within their stores.

Photo: Asian Trader

Photo: Asian Trader

Meanwhile, 8.7 per cent are actively expanding their ranges, while only 1.1 per cent reported reducing their offer.

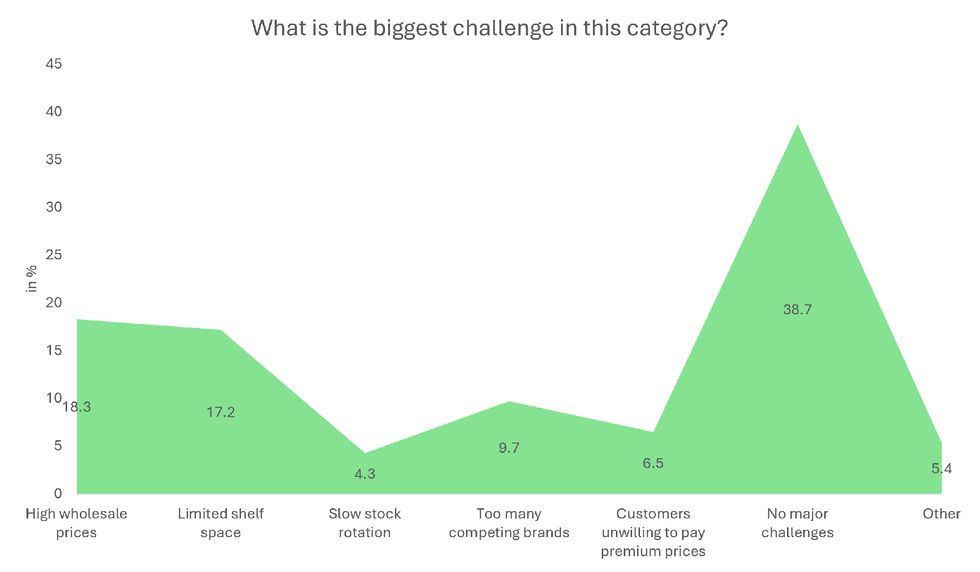

Few major obstacles

Retailers generally reported relatively few barriers to success.

Indeed, the largest single group of respondents (38.7 per cent) said they faced no major challenges in the category at all.

Photo: Asian Trader

Photo: Asian Trader

Where concerns were identified, high wholesale prices emerged as the most significant issue, cited by 18.3 per cent of retailers. Limited shelf space followed closely at 17.2 per cent, reflecting the ongoing challenge of balancing category growth with finite store space.

Other issues, including brand proliferation, premium pricing and slower stock rotation, attracted comparatively modest levels of concern.

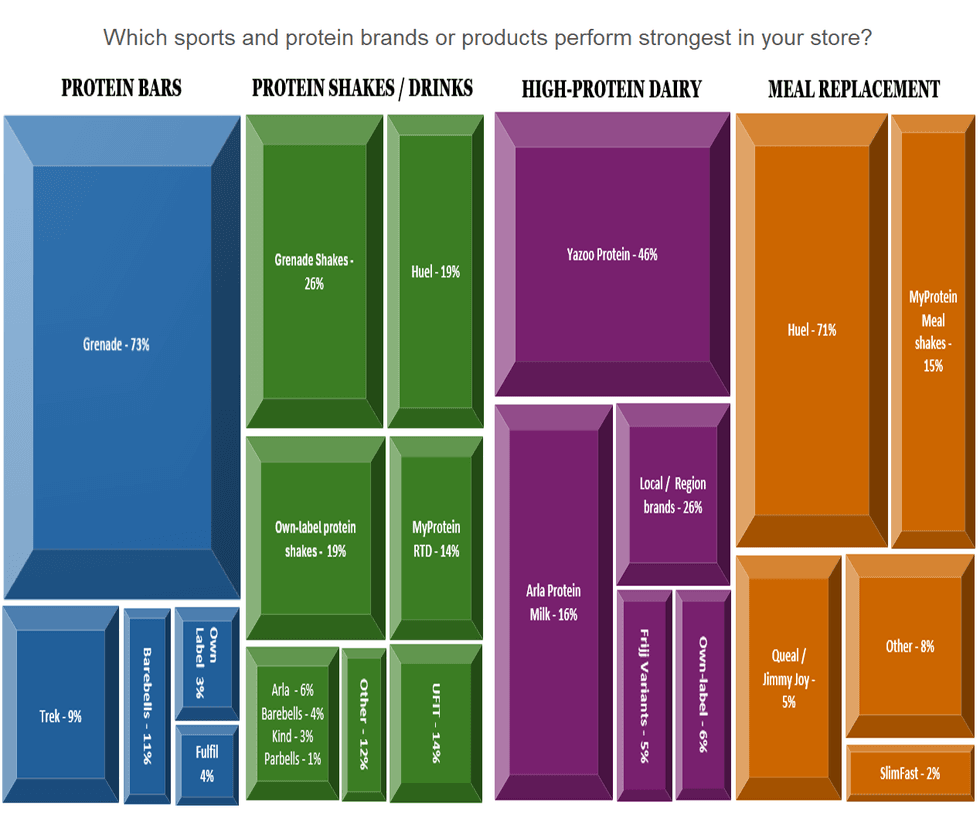

Category leaders emerge

When retailers were asked about top-performing products, several brands stood out.

Grenade was by far the dominant performer in protein bars, underlining the strength of its brand recognition and broad consumer appeal. The company also performed strongly within protein shakes and ready-to-drink products.

Photo: Asian Trader

Photo: Asian Trader

Within meal replacement products, Huel emerged as the clear leader, significantly outperforming rival brands and reinforcing its growing presence in convenience retail.

The survey also highlighted continued demand for high-protein dairy products, with established brands enjoying strong retailer support.