The latest retailer survey conducted for Asian Trader’s feature on beer, lager and cider offers a detailed snapshot of a category that is, on the surface, steady, but underneath reveals clear channel dynamics, pockets of growth, and ongoing competitive pressure. Drawing on responses from 118 retailers, the findings highlight not only overall trends but also important differences by store type that shape how the category is performing across the convenience landscape.

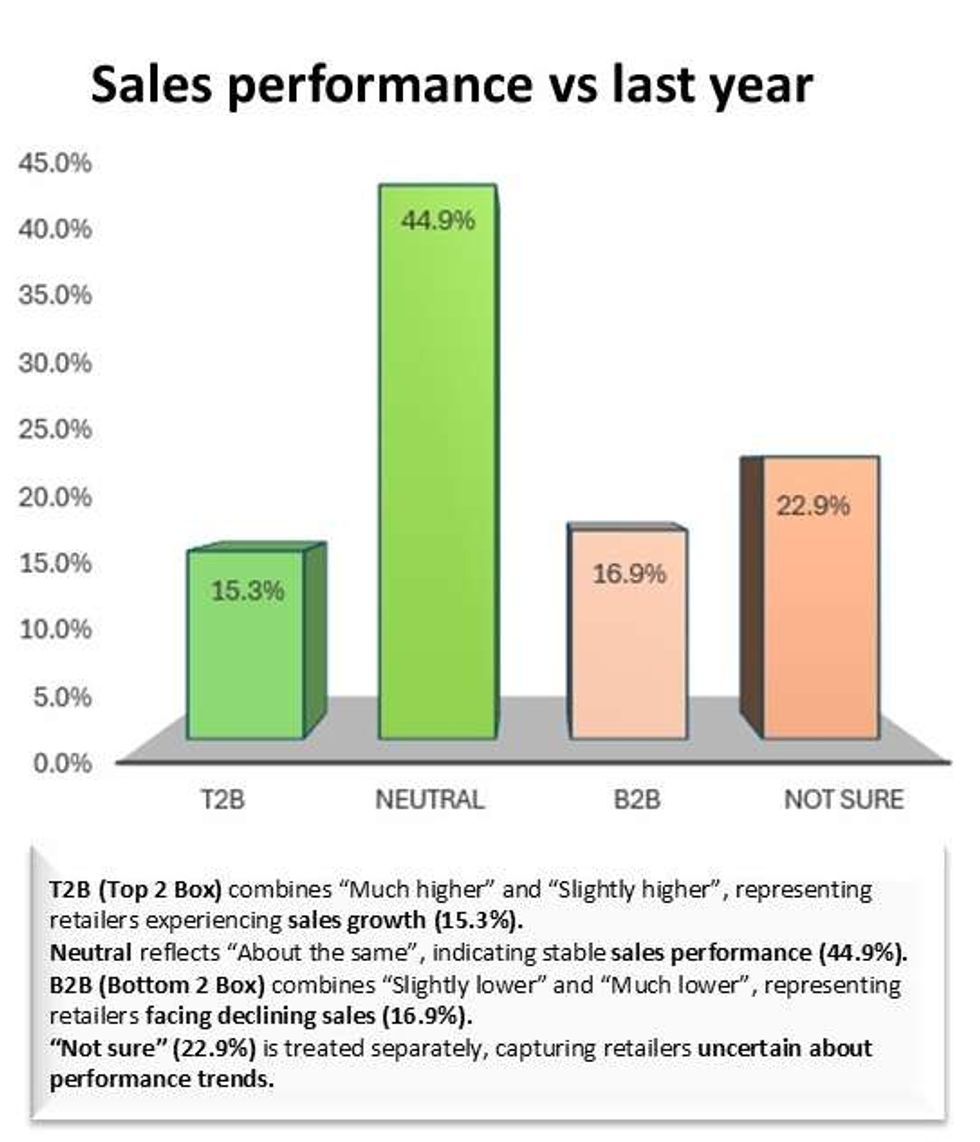

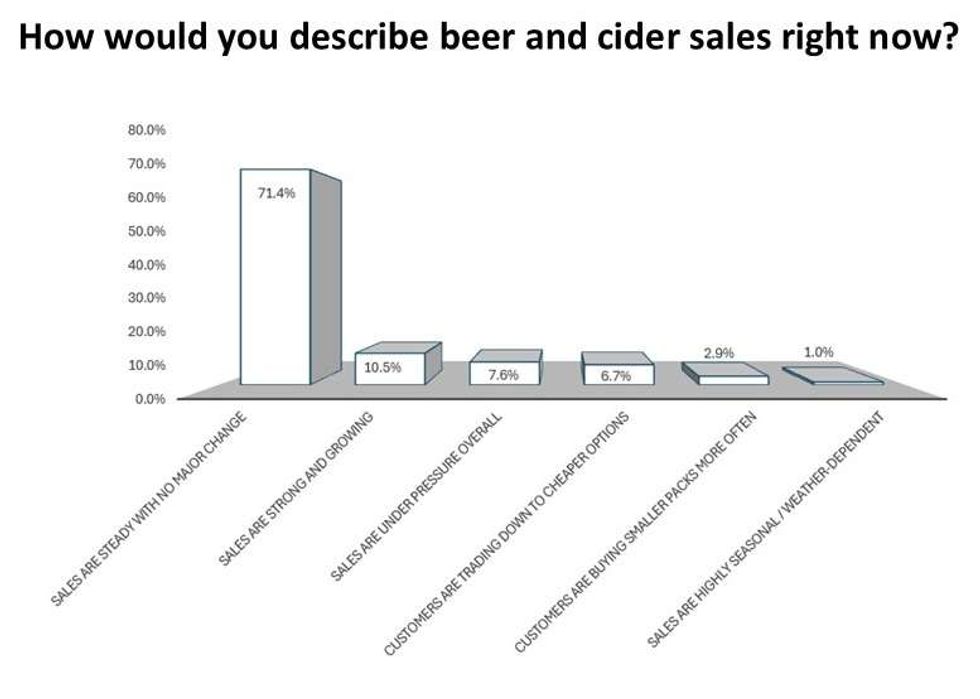

At a headline level, the category remains remarkably stable. Nearly three-quarters (71.4 per cent) of retailers describe beer and cider sales as steady, while 44.9 per cent say performance is “about the same” year-on-year. Growth is relatively modest, with 15.3 per cent reporting an uplift, compared with 16.9 per cent seeing declines. However, this topline masks a more nuanced picture when store formats are examined individually.

Photo: Asian Trader

Photo: Asian Trader

Forecourts and off licences stand out as the most positive channels, each delivering the strongest growth signals, with 27.8 per cent of retailers in these segments reporting increased sales. These outlets appear to benefit from a blend of convenience and mission-led purchasing, particularly as consumers continue to favour smaller, more frequent shopping trips. In contrast, petrol stations and supermarkets show weaker momentum. Petrol stations report the highest level of decline (40 per cent bottom-two-box), while supermarkets also show notable softness (20 per cent decline), suggesting that larger-format retail is facing more pronounced pressure despite its scale.

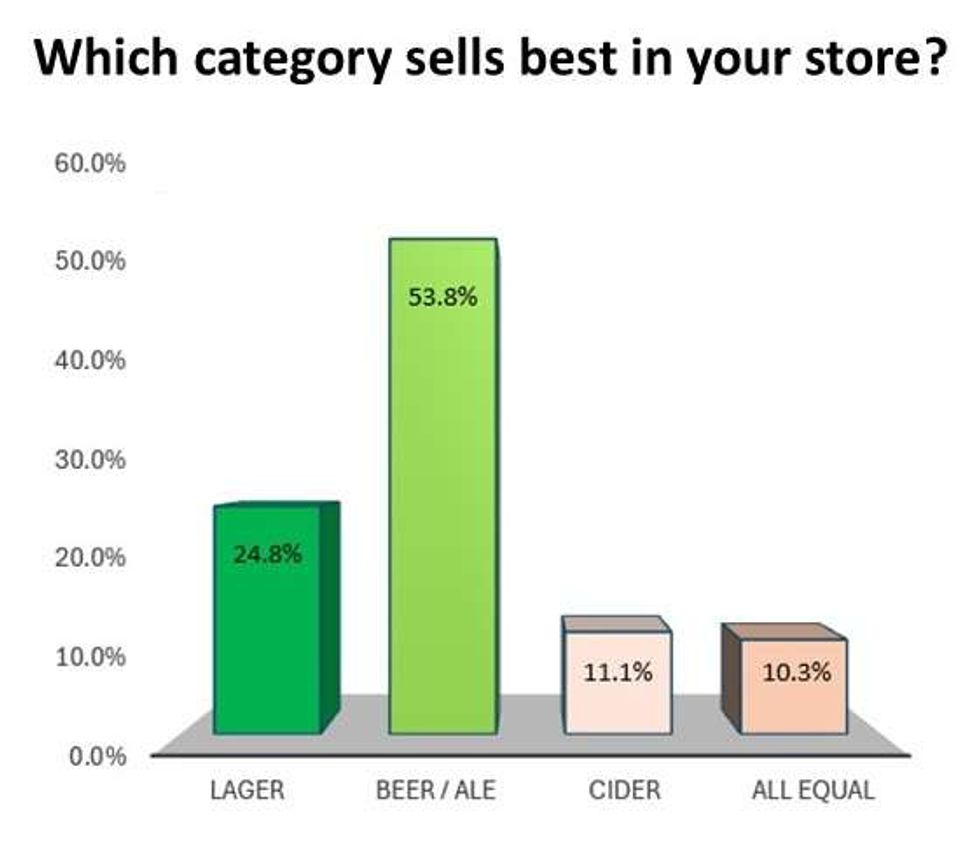

Category performance is also shaped by what retailers are selling. Beer and ale dominate decisively, with 53.8 per cent of retailers identifying it as their best-selling segment, more than double lager at 24.8 per cent. This dominance is especially pronounced in high-footfall channels such as forecourts (80 per cent), petrol stations (67.9 per cent) and supermarkets (55.6 per cent), reinforcing beer’s role as the backbone of the category in convenience retail. Lager, however, shows greater strength in more specialised environments, leading in wine merchants (50 per cent) and performing solidly in liquor shops (37.5 per cent) and off licences (30.8 per cent). Cider remains a secondary player overall, but with meaningful presence in liquor shops, off licences and supermarkets, where it accounts for around a fifth to a quarter of sales.

Photo: Asian Trader

Photo: Asian Trader

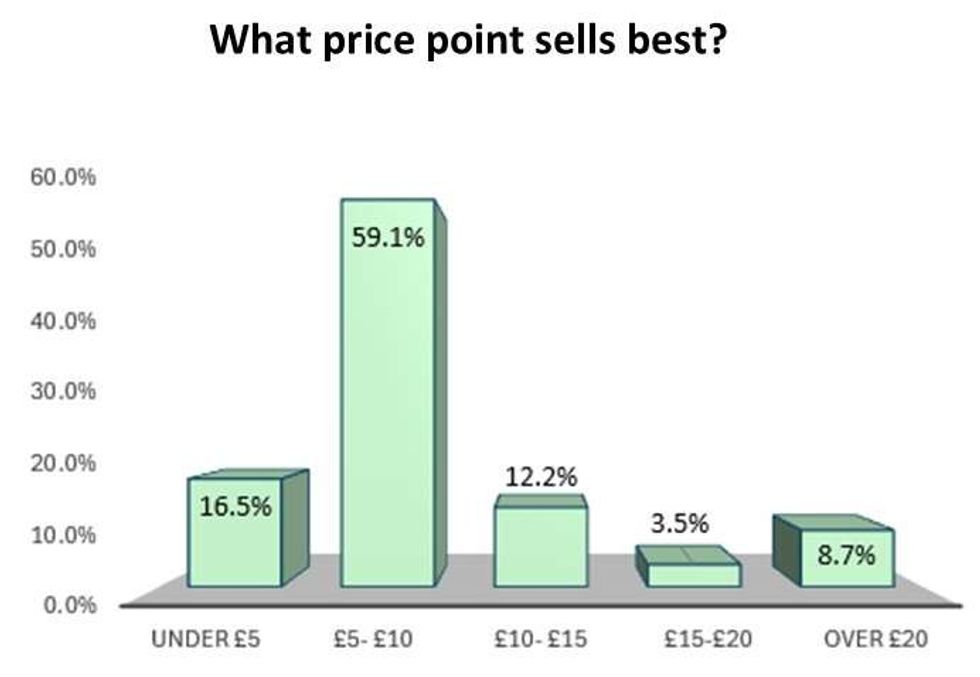

Pricing data further underlines the value-driven nature of the category. The £5-£10 bracket is overwhelmingly the sweet spot, cited by 59.1 per cent of retailers as the best-selling range. This holds true across all major store types, peaking in petrol stations (71.4 per cent), forecourts (70 per cent) and supermarkets (66.7 per cent. Lower price points under £5 retain relevance, particularly in petrol stations and wine merchants, reflecting impulse purchases and entry-level buying. Meanwhile, premium price tiers above £15 remain niche, though wine merchants and cash & carry operators show a greater skew towards higher-value sales, indicating more deliberate or bulk purchasing missions in those channels.

Photo: Asian Trader

Photo: Asian Trader

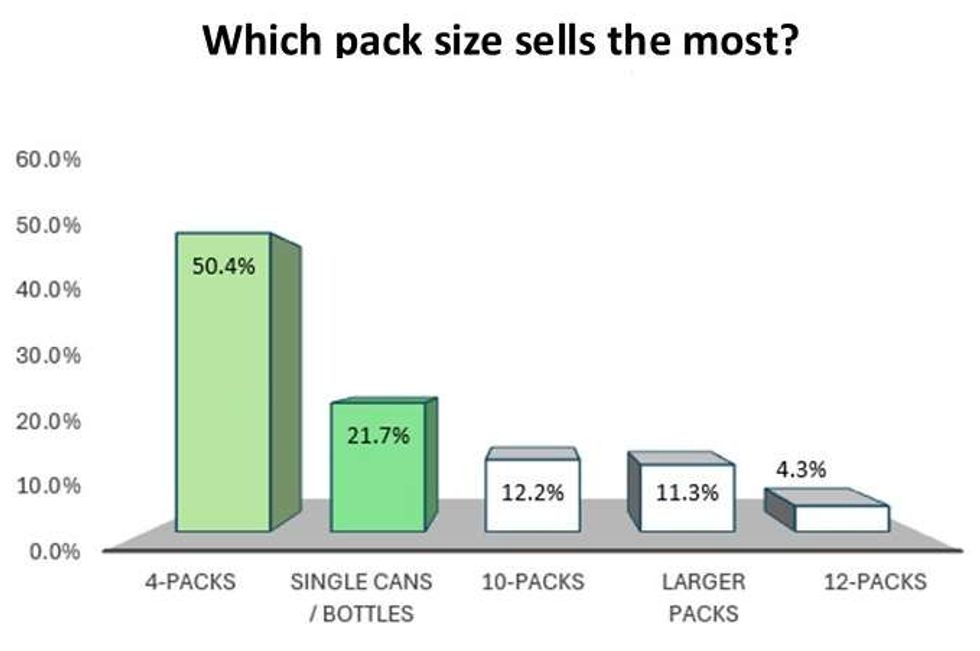

Pack size trends tell a similar story of balanced value and convenience. The four-pack is the clear winner, accounting for 50.4 per cent of top-selling formats and dominating across nearly every store type, including forecourts (80 per cent) and petrol stations (71.4 per cent). Single cans and bottles rank second at 21.7 per cent, highlighting the continued importance of immediate consumption and impulse purchases, particularly in channels such as wine merchants and tobacconists. Larger packs, while less prominent overall, gain traction in specialist and trade-focused outlets like wine merchants and cash & carry.

Photo: Asian Trader

Photo: Asian Trader

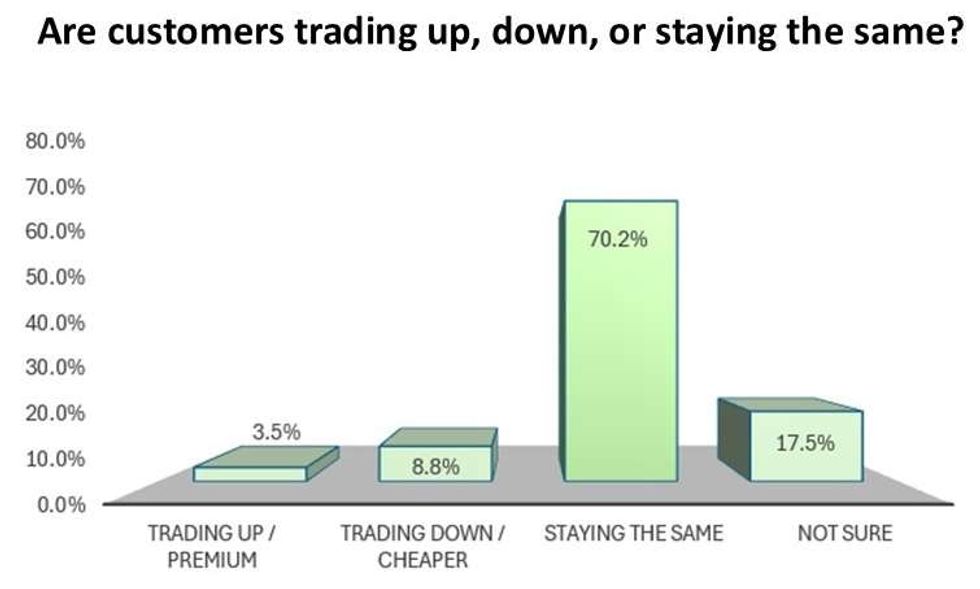

In terms of shopper behaviour, stability again emerges as the defining theme. A significant 70.2 per cent of retailers report that customers are “staying the same” in their spending habits. That said, there are subtle signs of pressure: 8.8 per cent of retailers note downtrading, compared with just 3.5 per cent seeing evidence of premiumisation. This suggests that while shoppers are broadly holding steady, there is a slight drift towards value-seeking. The pattern varies by channel, with supermarkets showing the highest stability (81.5 per cent), while tobacconists and petrol stations report more pronounced downtrading, reflecting the price sensitivity of their customer base.

Photo: Asian Trader

Photo: Asian Trader

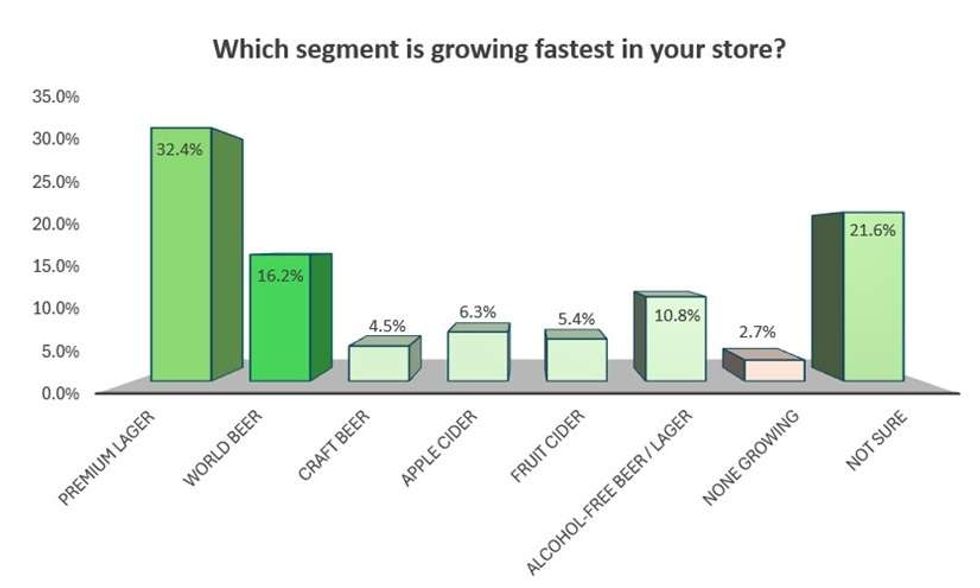

Where the category does show clearer momentum is in specific growth segments. Premium lager leads by a considerable margin, with 32.4 per cent of retailers identifying it as the fastest-growing segment. Its strength is particularly evident in off licences (61.5 per cent) and is consistent across supermarkets, wine merchants and petrol stations. World beer is the second key growth driver (16.2 per cent), performing especially well in petrol stations, liquor shops and forecourts, where shoppers appear more willing to explore international and speciality options. Alcohol-free beer and lager, while still relatively small (10.8 per cent), are gaining traction across multiple channels, pointing to a gradual shift towards moderation.

By contrast, craft beer remains niche, with limited but targeted appeal, while cider segments show only modest growth, with stronger relevance confined to specific outlets such as tobacconists.

Photo: Asian Trader

Photo: Asian Trader

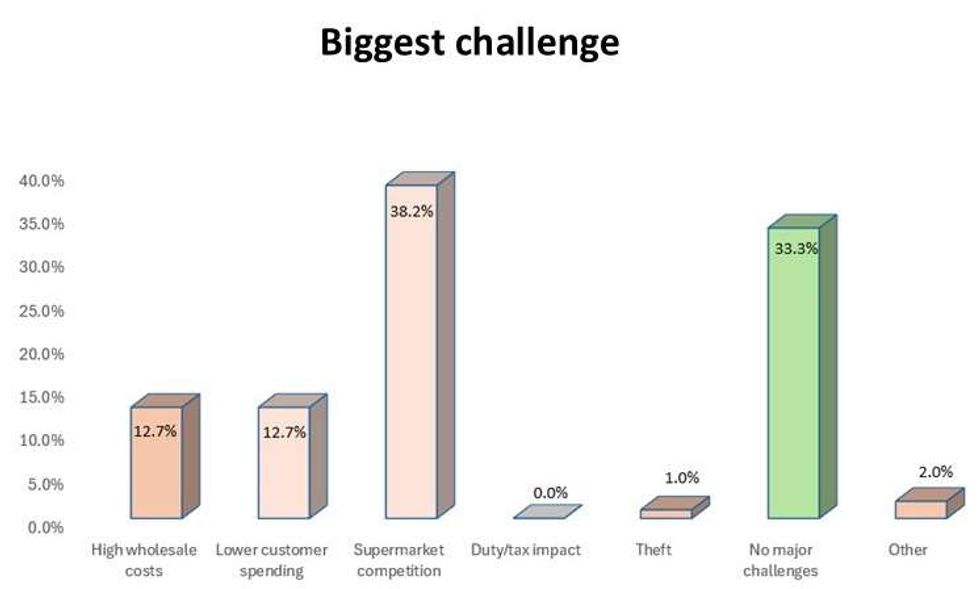

Despite these growth pockets, the category is not without its challenges. Supermarket competition is by far the biggest concern, cited by 38.2 per cent of retailers. This pressure is most acute in tobacconists, off licences, liquor shops and wine merchants, where price competition with larger chains is most direct. However, it is notable that a third of retailers report no major challenges, suggesting a degree of resilience within the sector. Cost pressures and reduced consumer spending are secondary concerns, each mentioned by 12.7 per cent of respondents, with the impact felt most strongly in petrol stations and supermarkets.

Photo: Asian Trader

Photo: Asian Trader

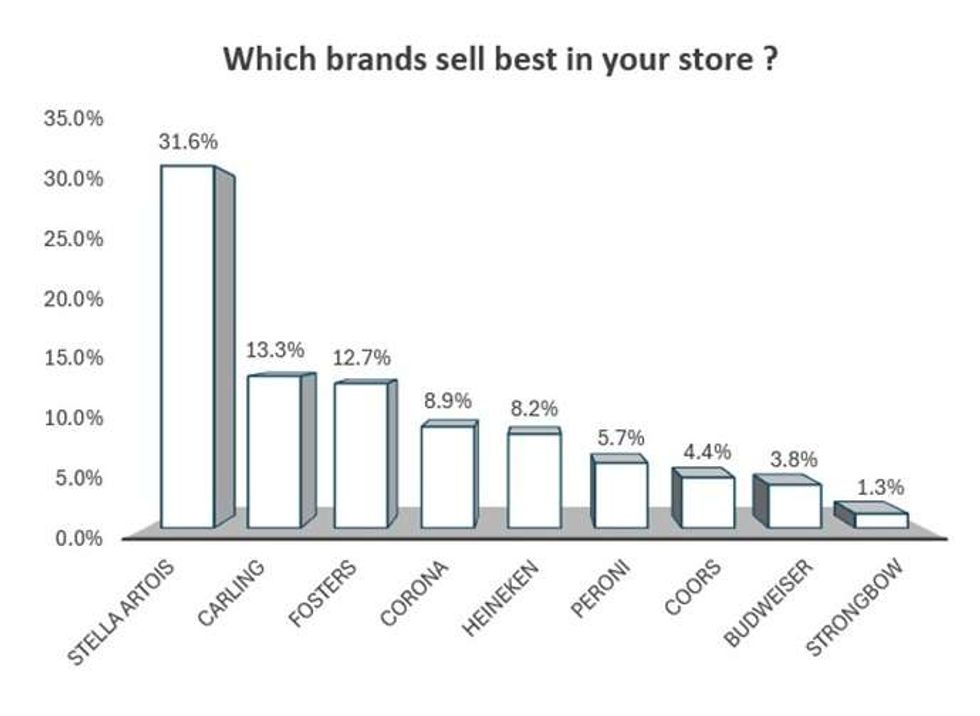

Brand performance reinforces the premiumisation narrative. Stella Artois leads the field with 31.6 per cent of mentions, followed by strong performances from Corona, Heineken and Peroni. Mainstream brands such as Carling and Foster’s continue to play a crucial role in driving volume, particularly in supermarkets, while petrol stations emerge as a balanced channel, performing well across both premium and value segments. Wine merchants, meanwhile, are heavily skewed towards premium and imported brands, underlining their role as specialist outlets.

Photo: Asian Trader

Photo: Asian Trader

Taken together, the findings paint a picture of a mature, stable category that continues to deliver consistent returns for retailers, even amid wider economic pressures. Growth is not uniform, but is instead concentrated in specific channels and segments, particularly premium lager and world beer. For convenience retailers, success in beer, lager and cider increasingly depends on aligning range, pricing and pack formats with the distinct missions of their store type, while navigating the ever-present challenge of supermarket competition.

Photo: Asian Trader

Photo: Asian Trader